The Time It Takes Athletes to Earn Their Pensions

When it comes to planning for retirement, no two professional leagues are the same.

Have you ever wondered what happens to the “below-average Joe” once he retires? You know, the guy that played for the league minimum for several years before calling it quits? What happens to them 5, 10, 20, or even 30 years after their careers end? Are they being financially supported by their former employer or are they working two jobs to support themselves and their families?

We often overlook this group of athletes, mostly because we fixate on the players that should earn enough money throughout their careers to be set for life. We expect athletes to have more money than god because the richest players are usually the most visible. Despite some well-documented cases of superstar athletes going bankrupt, we usually associate athletes with financial security because of earning potential of elite athletes, and tend to forget about the players that sat at the end of the bench or bounced from team-to-team and had to work hard just to crack a roster spot. They’re the kinds of players that depend on player pensions.

Thankfully for them, some North American sports leagues do offer a pension along with a 401(k). In other leagues, athletes are lucky to get one or the other. In all cases though, financial security is tied to service time, and while some players spend their careers chasing the greats, others are just hoping to hang around long enough to hit that magic number.

What follows is a break-down of the retirement plans for the seven major sports in North America, the requirements for earning a pension in each league and how these retirement plans differ across sports.

**The following numbers are all based on the most recent Collective Bargaining Agreements.

NFL

While players enter the NFL at a later average age than most leagues, they also leave it an earlier age too. The game has simply become too dangerous and debilitating to play for a long period of time and players are starting to fear for their safety. The average NFL career is about 3.3 years, with an average career salary of roughly $6.1 million. This means that for someone who starts his career at the age of 22, by his 26th birthday, chances are, he’s no longer in the league.

Primary Retirement Plan: Pension

Eligibility: The NFL bases their pension plan on ‘credited seasons’, meaning a season where a player is on an active/inactive roster and/or injured reserve for a minimum of three games. Players become fully eligible for benefits once they’ve amassed three credited seasons in the league.

Age of Withdrawal: At 55 years old, players can start collecting their pensions, although they do receive more annually if they wait longer to start collecting.

Payment: The NFL bases a player’s monthly benefit on the number of credited seasons they accumulated, and the time period of said seasons. Players received $660 per credited season every month for the 2015–2017 seasons, and will receive $760 per credited season every month for the 2018–2020 seasons.

Secondary Retirement Plan: Defined Contribution Plan (401k)

The NFL’s 401(k) retirement plan, also known as the Second Career Savings Plan, allows players to receive a 2:1 match, up to $26,000 once players have 2 credited season in the league.

Tertiary Retirement Plan: Annuity

The annuity plan is the last retirement benefit. Players can start cashing in on this benefit at the age of 35. According to the latest CBA, a player is eligible once he has four credited seasons. Once that mark is reached, the league will contribute $80,000 for every credited season from 2014–2017, and $95,000 for every credited season from 2018–2020.

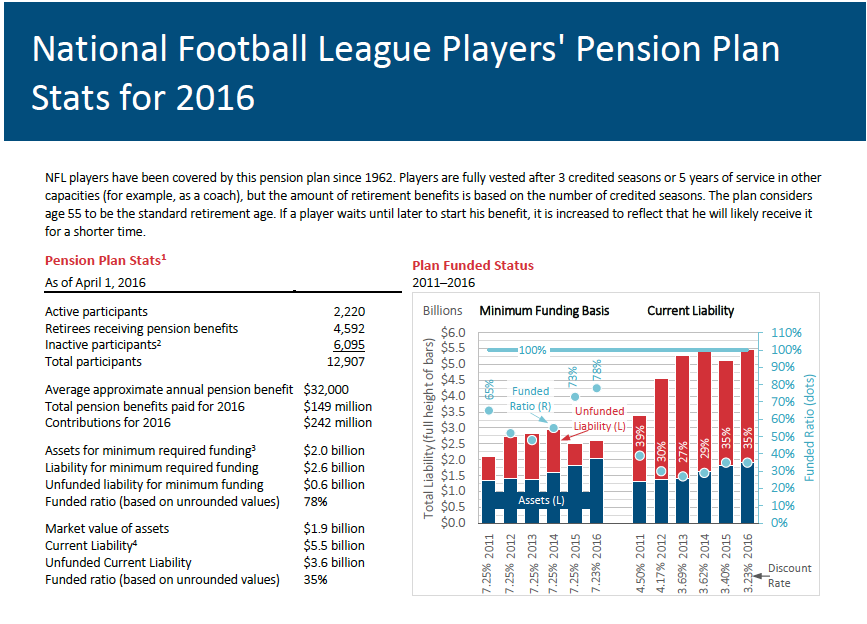

As you can see on the graphic above, the league has a lot of players to take care of, as they’re currently paying out pensions to around 4,600 retirees. That number is due to the larger roster sizes of NFL teams, and doesn’t factor in the reported $1B settlement the league paid to resolve several concussion lawsuits brought forward by retired players.

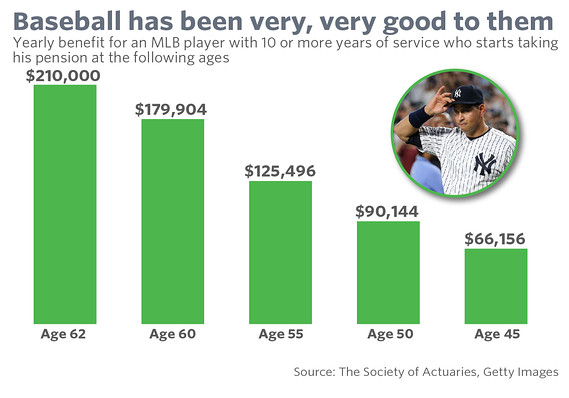

MLB

43. That’s the number of games that an MLB player must take part in in order to be qualified for a full pension. Since the average length of a players’ career is 5.6 years, most don’t need to worry about getting to that 43 (that is, as long as they escape from the minors). The average career earnings of a major league player is in the $18 million range, which is second only to the NBA.

Retirement Plan: Pension

Eligibility: Players are fully vested and are entitled to receive their full pension after only 43 games in the league.

Age of Withdrawal: To receive a full pension, the union recommends a player waits until the age of 62. However if he chooses, a player can start receiving reduced benefits once he turns 45.

Payment: This varies depending on how many years of service a player completed during his career. A player with 10 years of service qualifies for the maximum payment of $210,000/year.

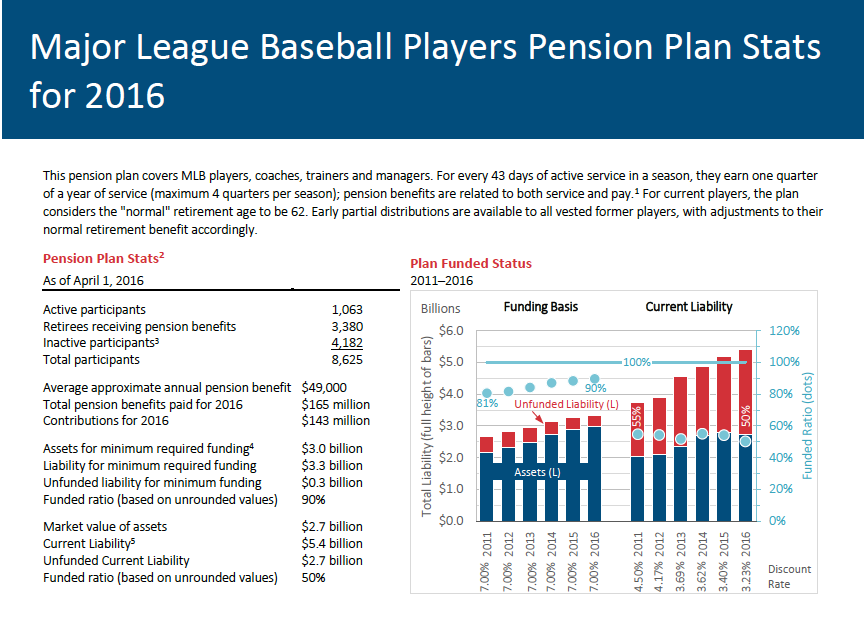

Major League Baseball has arguably the best pension plan for its players. In 2016 alone, they paid out a whopping $165 million in pension plan payments, with the average player receiving about 50k.

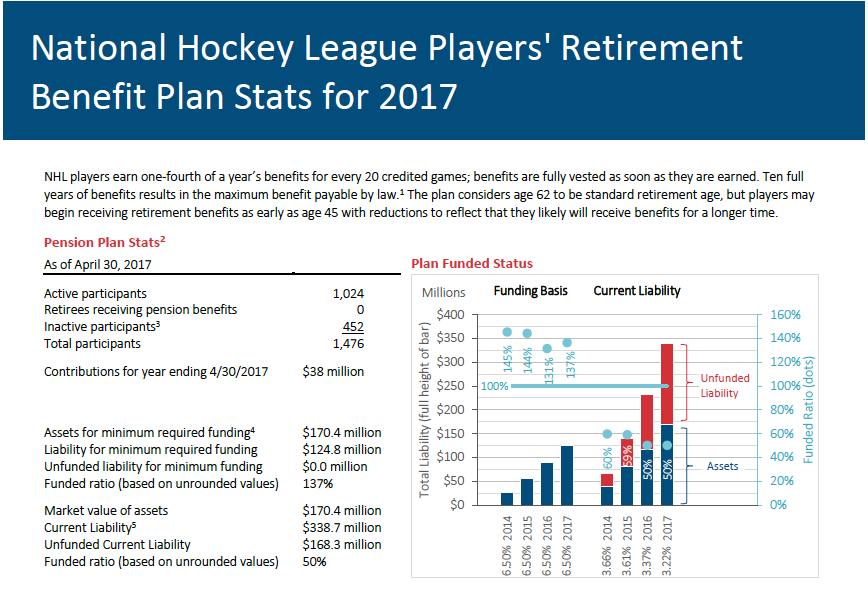

NHL

On average, NHL players earn approximately $13.6 million over the course of their careers, which last roughly 5.5 years. Of the big 4 leagues, NHL players have the lowest average career earnings, which makes the pension structure that much more important.

Retirement Plan: Pension

Eligibility: Players earn one quarter of a year’s benefits for every 20 credited games, and they are vested in their benefits as soon as they earn them. A player who has earned 10 full years of benefits will have earned the maximum benefit payable by law.

Age of Withdrawal: A player can start receiving their full benefits at 62, but can choose to start receiving reduced payments at the age of 45.

Payment: The plan is based on the amount of service time players accumulate over the course of the CBA, and has a maximum yearly value of $255,000.

MLS/WNBA

Retirement Plan: Defined Contribution Plan (401k)

The MLS and the WNBA currently do not have a pension plan program that is comparable to the other leagues. Players are able to contribute to their 401(k), and it is capped at the amount allowed by the IRS and varies from year to year($18,000 for 2018).

In the MLS, team contribution is capped at $50,000 per year.

For the WNBA, “employers contribute up to 25% of the amount of employee deferrals. Other team contributions include: 2% of base salary for a player with two years of experience; 3% for those with three years; and 4% for those with four years or more.”(Source)

I know what most of you will say, ‘ the revenue is much lower and they simply can’t afford it’. I understand that, I do, but taking care of your athletes should be priority number one, and committing to the long-term financial security of your athletes will only encourage more athletes to pursue pro careers in these leagues. If I’m leading the players union of either league, I’m not walking out of the next CBA negotiation without securing a pension of some kind.

PGA Tour

Retirement Plan : Pension (Merit-based)

The PGA is on another level when it comes to their pension plans — golfers receive money in their pension accounts based on three criteria:

- The number of cuts they make.

- Their performance in each of the three schedule segments throughout the season.

- Their position on the end of the season money list.

When it comes to the cuts-made, “a player must make 75 cuts to be 50-percent vested and is fully vested at 150 cuts”(Source). To be fully vested in the three segments portion of the plan, players have two options; they can either play in 100 official tour events in four years, or play each event on tour once over a four-year period. The money earned for position on the end of season money list is fully vested immediately. The PGA is very generous, many golfers will have millions of dollars in pension money by the time they retire.

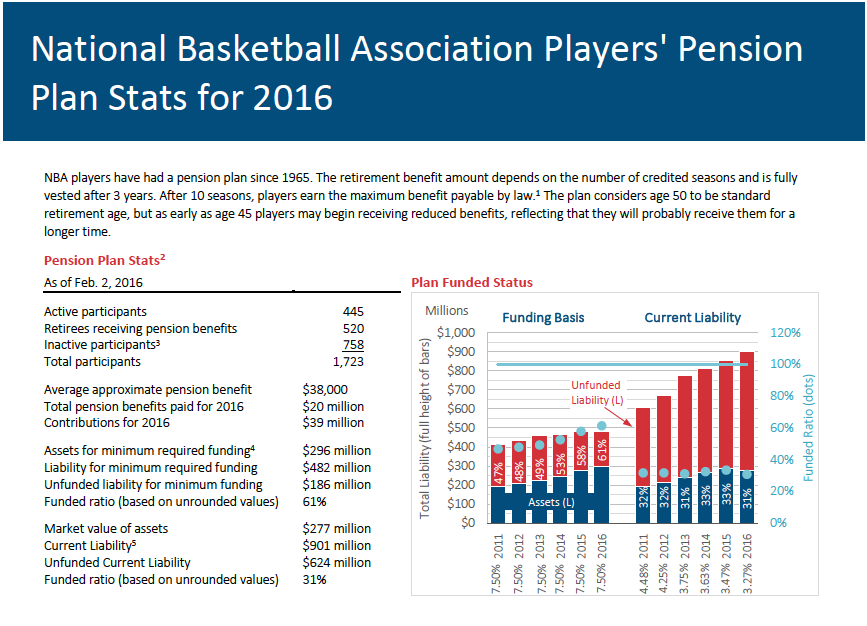

NBA

NBA players have the highest average career earnings at $24.8 million, to go along with an average career length of 4.8 years. Despite these lofty numbers, the NBA has made financial literacy a huge priority for rookies in recent seasons, to help them better understand the opportunities and pitfalls of such earning power.

Primary Retirement Plan: Pension

Eligibility: In order to be eligible to earn a fully-vested pension, a player must complete 3 NBA seasons. A player will be credited with one season of NBA service when he is on either the NBA Active or Inactive list for one or more days during the regular season.

Age of Withdrawal: A player can start cashing-in once he turns 45, but, as with several other sports, a player can only earn their maximum pension if they wait to start collecting until the age of 62.

Payment: If a player with the minimum service time starts collecting at 45, they’ll receives a payment of about $19,000 annually. With a decade of playing time, that rises to $60,000. If they decide to be patient and are in no rush to receive payments until they’re 62, those numbers amount to $60,000 and $200,000 respectively.

Secondary Retirement Plan: Defined Contribution Plan (401k)

NBA Players are also eligible and encouraged to participate in a 401(k) plan, in which team contributions can be greater than player deferrals.

So, if you’re a young, multi-sport athlete, which sport should you lean towards if you want to be quickly eligible for a lifetime pension? With only 43 games of service time necessary to qualify — and the fact that the MLB schedule allows for you to accomplish that within the first two months of your career —baseball is you best bet. Get-in, get-out, avoid getting hurt, and simply wait until you’re 45 to start cashing cheques. If you’re looking to receive the maximum lifetime pension though, golf should be your sport of choice. No other pension will ever sniff the amount that top-end golfers will receive in retirement funds.

Whatever sport you might choose though, what’s clear is that having some sort of pension plan is crucial for pro athletes, seeing as players are only one life-altering-injury away from never playing again. While most leagues do offer some form of long-term financial security for its players, others like the MLS and WNBA still lag behind. It’ll be on those unions to find solutions and answers going forward, to make sure their athletes are truly protected for life.

Afi Ahmed is a writer and podcast host at Grandstand Central. He is also known as the ‘King of Hot Takes’, a title which he bestowed upon himself, against the wishes of his fellow GSCers. You can follow him here.

Understanding why some athletes perform in the clutch, while others come up short.grandstandcentral.com